Products will be low-volume and high-cost modules for 5G and high-volume and low-cost modules for NB-IoT and LTE – M applications. The latter will replace the 2G/3G devices currently deployed.

This growth will lead to a market value of over $800 million at the RF front-end level.

Cellular IoT will benefit from 5G deployments through private networks with either private or public frequencies, and public networks. Larger deployments will be seen in China, the U.S. and Europe with a high 5G SA penetration rate.

Only a few companies have the capability to develop 5G modules. Qualcomm is the first company offering a commercial chipset for 5G. For NB-IoT, the price point is lower, but stays too high for any small entrant.

Multiple approaches have been tried in the past to develop the IoT. They have used unlicensed frequencies, through protocols like the IEEE802.15.4 based Zigbee or Z-Wave, the LoRaWAN and Sigfox protocols, or long-range Wi-Fi. But this has not been a success, mainly due to the general requirement for data reliability and security, meaning confidentiality, integrity, and availability.

But this is changing now with cellular protocols aimed at IoT. These cellular protocols range from the low data rate NB-IoT to the very high data rate, high reliability, low latency 5G Cat20. The latter has finally started to see traction from the industry.

“Cellular deployment is expensive, either on a capital expenditure standpoint for private networks or an operating expenditure standpoint when using public networks. But 5G offers unprecedented capabilities in terms of data security, creating a market opportunity for critical applications,” says Yole’s Cédric Malaquin, “these are niche applications, for example, in highly automated industrial environments, where wireless connectivity adds a lot of value. Other applications range from machine vision to autonomous guided vehicle monitoring. They are now motivating investment in 5G deployments, thus opening the market for all other cellular-based deployments to come”.

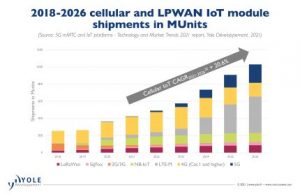

Market volume is expected to reach 900 million devices in 2026. It started in 2020 with a volume of 298 million units driven by the replacement of 2G/3G devices like points of sale or telematics.

These volumes are still very far from the billions of industrial connected devices anticipated by tech companies several years back. This is mostly due to the niche nature of IoT applications. But this still represents a big market opportunity, reaching $859 million in 2026 from $257 million in 2020 with a 22.3% CAGR for 2020-2026 at the RF front-end component level.

Yole’s analysts expect to see increased use of cellular IoT in 2023 thanks to worldwide deployments of true 5G public networks, using standalone 5G, permitting network slicing.

They also expect to see a new RF module offering in 2023, given that today the only solution is provided by Qualcomm at a quite expensive cost. Developments are awaited from other players, like Sequans Communications.

Qualcomm will also soon release its second generation of 5G modules, expected at half the price of its current solution. The IoT industry needs this diversification and strengthening of supply.

By 2023, Yole sees also more private networks deployments. Whereas today they are starting at pilot level and are meant for high-value applications. But, once deployed, they are expected to be used for lower value IoT applications, especially those using LTE-M or the future NR-Light protocols.

Therefore, the future ramp-up of IoT is expected through the conveniently timed conjunction of events at public network, devices, and private network levels for 2023.

Once this cellular IoT adoption happens, the democratisation of the technology will finally take place. It will be followed by industrial consolidation in the longer term, and ubiquitous use of the licensed radio frequencies for non-consumer purposes.