Annual GaN power devices revenue for 2021 will reach $83 million – a 73% YoY increase, says TrendForce.

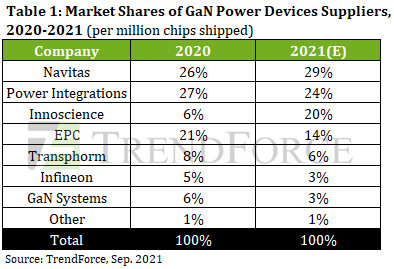

Navitas is projected to obtain a 29% market share (measured by total shipment) and overtake Power Integrations (PI) for the top position this year.

Thanks to Navitas’ proprietary GaNFast power IC design and great relationships with its partners in the Semiconductor supply chain, it has become the largest supplier of GaN power IC chips in the consumer electronics markets.

The company is currently partnering with leading global smartphone and PC OEMs, including Dell, Lenovo, LG, Xiaomi, and OPPO.

Given the rising demand for Navitas’ fast charge ICs from clients this year, the company is expected to transition its chip orders in 2H21 from TSMC’s Fab 2, which is a 6-inch wafer fab, to other 8-inch fabs instead, in order to resolve the issue of insufficient production capacity.

At the same time, Navitas is also targeting SAIC (Xiamen Sanan) as a potential supplier of foundry services. Navitas will likely target the data centre market first by releasing related products in 2022.

Pi was the longtime leader in the GaN power devices market. For this year, PI has released the latest InnoSwitchTM4-CZ series of chips, based on its proprietary PowiGaNTM technology. In addition, PI’s recently released integrated AC-DC controller and USB PD controller ICs are expected to be major drivers of PI’s revenue growth this year.

With an estimated 24% market share, PI will likely take the runner-up spot in the ranking of GaN power devices suppliers for 2021.

The market share of China-based Innoscience is projected to rise to 20% this year, the third highest among GaN suppliers. Innoscience’s performance can primarily be attributed to the massive spike in its shipment of high-voltage and low-voltage GaN products.

In particular, Innoscience’s GaN power ICs, used for fast chargers, are now entering the supply chains of tier-one notebook manufacturers for the first time ever.

The Chinese government has been increasing its support of its domestic compound semiconductor industry, investing in about 25 projects aimed at expanding the domestic production capacity of compound semiconductors in 2020 (excluding GaN-based optoelectronics materials and devices). These projects totalled more than RMB¥70 billion, a 180% YoY increase.

Although the technological gap between China and its global competitors is fast narrowing, China is still noticeably inferior in terms of monocrystalline quality, resulting in a relatively low self-sufficiency rate of high-performance SiC substrates.

TrendForce’s data indicate that, as of 1H21, about seven production lines have been installed in China for GaN-on-Si wafers, while at least four production lines for GaN power devices are currently under construction, also in China.

On the other hand, China possesses at least 14 production lines (including those allocated to pilot runs) for 6-inch SiC wafers.