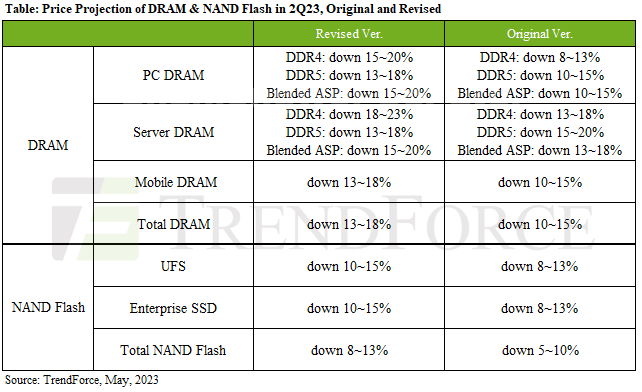

DRAM prices are projected to fall 13~18%; NAND Flash is expected to fall between 8~13%.

The drop in DRAM prices was mostly attributed to high inventory levels of DDR4 and LPDDR5 as PC DRAM, server DRAM, and mobile DRAM collectively account for over 85% of DRAM consumption. Meanwhile, the market share for DDR5 remains relatively low.

The ASP of PC DRAM is expected to decrease by 15~20% in 2Q23.

The for server DRAM will remain between 15~20%.

The ASP decline of mobile DRAM to expand to 13~18% in 2Q23.

NAND Flash is primarily affected by enterprise SSD and UFS which account for over 50% of total NAND Flash consumption.

The Q2 ASP decline of enterprise SSDs will be 10~15%.

The Q2 ASP decline of UFS will be 10~15%.

View more : IGBT modules | LCD displays | Electronic Components